5 Goals for Personal Finance and Planning

Financial goals help savings grow by ensuring you have a healthy basis for your future plans. While having a healthy savings account is ideal, factors like building credit, investing and compiling retirement savings are also important for personal finance.

What Is a Financial Goal?

A financial goal is an objective or plan that involves building financial literacy and managing your money. Most often, financial goals involve saving money for a purchase of some kind, but a constructive goal may also involve building credit, investing or even earning more money.

Why Is Personal Finance Important?

Tracking and managing your money is integral to your future success. The benefits of financial management include mitigating that stress and the ability to:

- Pay off debt: The average U.S. household that has debt owes around $145,000 from sources such as credit card debt, car loans, student loans and mortgages. Even the youngest generation, ages 18 to 23, already has an average of $16,043 in debt.

- Build retirement savings: When you’re young, it is easy to put off saving for retirement, but having money set aside is integral to having a good quality of life as you age.

- Stay within your budget: Spending beyond your means can lead to high accumulations of debt, causing stress and anxiety. If you budget and set goals, you can stay comfortably within your means.

- Have emergency funds: Having an emergency fund is essential to prepare for unexpected surprises. With an emergency savings fund, you can be prepared for medical bills, home or vehicle repairs and other unexpected expenses.

Setting yourself on a secure financial footing will allow you to achieve your personal goals and build an enjoyable and healthy life.

Types of Financial Goals

Examples of smart financial goals will depend on your situation. You might want to save a few hundred dollars for a new tablet or laptop, or a few thousand to buy a used car. In general, there are three types of financial goals:

Short-Term Financial Goals

Short-term financial goals can be met in a year. Examples of short-term goals include vacations, small home improvements and electronics like televisions and laptops.

Mid-Term Financial Goals

Accomplishing something within the next five years is a mid-term financial goal. Setting goals like this might involve more planning and preparation. Examples of mid-term financial goals include improving credit scores, saving for a car payment, installing a pool or paying off a credit card.

Long-Term Financial Goals

A long-term financial goal would take longer than five years to accomplish. Examples of goals that you’ll work toward over a number of years include purchasing a house, saving for retirement, or starting a college savings account for your children.

5 Examples of Goals for Personal Finance

While everyone is different and has different desires, these financial goal examples are common objectives many people have to improve their personal financial health.

1. Start Budgeting

The essential purpose of a budget is to ensure you live within your means, and it’s helpful when setting money aside for future expenses.

Many people think of budgeting as something that involves strict calculations and spreadsheets, but most families take a more general approach. Subtracting your average expenses from your income can be a good start, but a stricter budgeting plan might involve setting aside specific sums of money for certain expenses.

Monthly expenses, including bills, housing and food, for the average family of four might total around $7,095. Calculate your own expenses over a few months to create a budget for food shopping, entertainment and extras so you stay within your means.

2. Build Your Savings

Another goal you might set for yourself is to set aside money in a savings account. Savings allow you to prepare for both expected and unexpected expenses. Your income will dictate how much you can save.

The amount you save will depend on your goal and time frame — someone saving up for a house will have to put away more money for a longer period than someone saving for a car. If you’re simply saving for a summer vacation, you might start in the fall and save until the summer months when you book your trip.

No matter what your savings goals are, having a clear plan and staying disciplined are important. The most common savings strategy is to open a separate account and transfer money there. A budgeting goal can work in tandem with growing your savings, as staying within or under budget can give you more money to save.

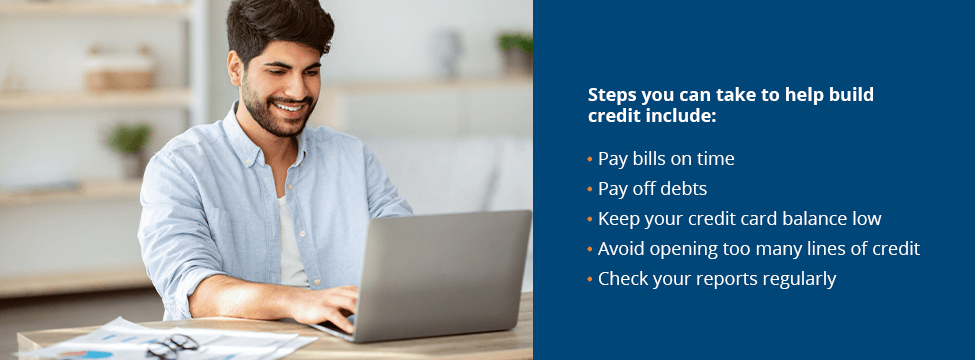

3. Improve Your Credit

Building credit can impact future financial goals like buying a car or house. People with a good credit score demonstrate good history with payments, debt and credit history, so lenders will be more likely to offer favorable loan terms and credit requests.

Steps you can take to help build credit include:

- Pay bills on time

- Pay off debts

- Keep your credit card balance low

- Avoid opening too many lines of credit

- Check your reports regularly

4. Save for Retirement

Having a healthy retirement plan starts a long time before you retire. There are a few options when it comes to retirement savings.

Many employers offer a 401(k) plan. Some even offer matching options, meaning they will contribute a percentage of their employees’ contributions throughout the year. Individual retirement accounts (IRAs) and Roth IRAs are other retirement savings accounts that can be good options for people. Some also invest their money in stock as a backup retirement savings account.

5. Pay off Debt or Loans

Paying off debts and loans is an important financial goal because it may impact your ability to get a mortgage or make purchasing a car more difficult. Clearing your loans can also improve your quality of life as you’ll have less stress and more expendable income to do things you want to do, like vacations and home improvement projects.

Student loans are often a major source of debt. The average federal student loan debt currently stands at $36,510 per borrower, and even 20 years after graduation, almost half still owe over $20,000. It’s important to do research before taking on student loans or loans of any nature to ensure you’ll be able to pay them off in the future.

Improve Your Personal Financial Health With Mid Penn Bank

Responsible financial management includes saving, budgeting, investing and planning for unexpected expenses. With the professional financial services at Mid Penn Bank, you can work toward personal financial health. Because Mid Penn Bank is a community bank, we are invested in the individuals who make up our community.

Share:

Disclosures

The material on this site was created for educational purposes. It is not intended to be and should not be treated as legal, tax, investment, accounting, or other professional advice.

Securities and Insurance Products:

NOT A DEPOSIT | NOT FDIC INSURED | NOT BANK GUARANTEED | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | MAY LOSE VALUE