How to Manage Your Monthly Bills

Jump ahead:

Make a Monthly Spending Plan to Help Manage Bills

1. Make a List of Your Monthly Bills

2. Make a List of Monthly Expenses

3. Understand Your Income

4. Prioritize Your Bills

5. Schedule Your Bills

6. Use Tools to Manage Your Income and Expenses

Tips to Help You Manage Your Bills

1. Create a Physical Space for Managing Your Bills

2. Figure out How to Handle Irregular Expenses

3. Use Cash When You Can

4. Talk to Your Partner about Financial Matters

Managing Your Monthly Expenses and Bills Helps Set You up for Financial Success

When a bill comes due, you pay it. It seems like it should be simple enough, right? Often, things that seem straightforward can turn out to be the most complex. Managing your bills can be a breeze, if you only have one or two of them each month and if their total cost is considerably less than your income. If that’s not the case for you, what’s the best way to pay your bills each month? With a bit of planning and prioritizing, you can get a handle on your monthly bills and expenses.

So how do you keep up with monthly bills? Learning how to manage your bills and expenses means fewer missed payments, reduced late fees and no more having to explain why you made a late payment. Here’s what you can do to organize your bills and make late or missed payments a thing of the past.

Trouble With Expenses? Contact Us!

Make a Monthly Spending Plan to Help Manage Bills

When learning how to manage bills, a monthly spending plan is a great place to start. Your monthly spending plan lets you see at a glance where your money is going to go during a month. It also helps you see how much money you have coming in from your job or other sources of income. With a monthly spending plan, you can see how much you have left over after you pay all your bills for other expenses, such as groceries, clothing and household care. You can also get a sense of how much money you can contribute to your financial goals, such as saving for retirement or building up a down payment for a home.

Making a spending plan involves three steps.

1. Make a List of Your Monthly Bills

The first thing to do when making your spending plan is to list all your monthly bills. At this point, only look at bills that arrive regularly or that are for a generally fixed amount. Regular bills often include:

- Rent or mortgage

- Electricity

- Gas

- Water and sewer

- Internet/cable/phone

- Subscription services, such as a gym membership, newspaper, Netflix or Hulu

- Credit card bills and loan payments

- Insurance

Also consider that your list of bills to pay when owning a home may look different than if you rent.

2. Make a List of Monthly Expenses

In addition to your monthly bills list, you most likely have other expenses that pop up during the month, and that tend to vary. These additional monthly expenses often include the cost of groceries, clothing, transportation and entertainment. You pay for these items as you need them, so it can be more challenging to remember to leave space for them in your spending plan.

Estimating how much variable expenses there will be each month will help you get on top of paying your bills and avoid coming up short. Some everyday variable expenses to make room for in your spending plan include:

- Groceries

- Clothing

- Gasoline or other transportation costs

- Beauty and personal care products

- Household products

- Medications and health care

- Pet care

- School costs for yourself or your children

- Entertainment

- Dining out, including snacks and coffee on the go

- Savings

Since variable expenses can fluctuate from month to month, it can be tricky to figure out how much money to set aside for each. One option is to look at your spending from past months and figure out the average amount you spent in each category. You can adjust it as needed based on your needs and spending during a given month.

3. Understand Your Income

The third step when putting together a spending plan is to understand how much money you have coming in monthly and when you get paid. If you get paid monthly, biweekly or weekly, that will influence how you pay your bills and the schedule you follow.

If you get paid once a month, you need to make that money stretch from day one up until day 30. If you get paid twice a month, you can dedicate your first paycheck to bills that are due early and the second paycheck to bills due later in the month.

Some people don’t receive paychecks regularly. Instead, they get commission after a sale, or they get paid after finishing a project. While that can make it difficult to predict when you’ll get paid and challenging to plan for monthly expenses, it doesn’t make it impossible. If you get paid irregularly, one way to streamline your budget and manage your bills is to live on last month’s income. That way, if a client is late making a payment or a commission check gets delayed, you’ll still be able to pay your bills.

It’s also a good idea to get a firm grasp of how much money you have coming in monthly and how that income compares to the cost of your bills and other expenses. You might realize your income is less than all of your expenses, which could explain why you’ve been having difficulty managing your bills. If that’s the case for you, you have a few options.

Option one is to find a way to live more frugally. You can try switching to a less expensive phone plan, cutting out specific subscription services or shopping around for a different electricity supplier. In Pennsylvania, you can choose which supplier provides electricity to your home, which can mean you end up paying a lower price.

The second option is to find ways to increase your income each month. You might take on a side hustle, ask for a raise or find a part-time job if your schedule allows.

4. Prioritize Your Bills

Life has a way of surprising you, and there might be months when you can’t pay all your bills in full. If that should happen, what are your options? Part of learning how to manage your bills on time means prioritizing your expenses based on necessity. This strategy will help you decide what to cut back or out when money is tight.

What’s the best way to prioritize bills? While there is some variation, your best bet is to focus on paying any bill that will keep a roof over your head and that will provide you with the necessities of life. Pay your mortgage or rent first, followed by water, electricity and gas. Refinancing your mortgage can offer ways to decrease the monthly payment.

When money is tight, you might want to eliminate non-essential bills. You can switch off cable or internet at home for a few months or switch to a cheaper cell phone plan.

Some bills offer more flexibility than others. If you’re going through a period of financial difficulty, you might switch to making the minimum payments on a credit card or other loan, rather than paying in full or paying more than is due. Paying the minimum will mean you end up paying more interest over time, but it’s a better option than paying late or not paying at all and having that affect your credit.

If you find you absolutely can’t pay a bill and it’s not a high priority, call the company and explain your situation. In some cases, you might be able to work with the company and come to an agreement about your bill or get help paying the bills based on your income. It never hurts to ask if there are payment programs available, or if you can work out a payment plan during a period of financial difficulty.

Programs such as LiHEAP provide financial assistance to households that earn below specific amounts and who need help paying their energy bills. Your utility company might also offer a program such as budget bill pay, which calculates the average of your bills over 12 months and can help you better predict what you’ll need to pay monthly.

You can also look for ways to reduce your variable expenses each month if paying your fixed bills becomes a challenge. One of the first places to look might be at your grocery spending. While food can be expensive, there are also lots of inexpensive, healthy options available. When things are tight, you might switch from fresh vegetables to frozen, which are just as nutritious and cost less. You might also consider making more meals based on beans and whole grains and reducing the amount of meat you eat.

5. Schedule Your Bills

When should you pay your bills? The answer depends on two things.

- When you get paid each month

- When the bills are due

Aim to pay the bills by their due date, but make sure you have the funds in your bank account first. If your bills and paychecks don’t line up, you can contact each company and ask to adjust your bill due date. Many companies are happy to change your billing schedule if it means you are more likely to pay by the due date.

Arranging your bills so they are all due at the same time each month also helps streamline your process and can make you less likely to overlook a bill or miss a payment.

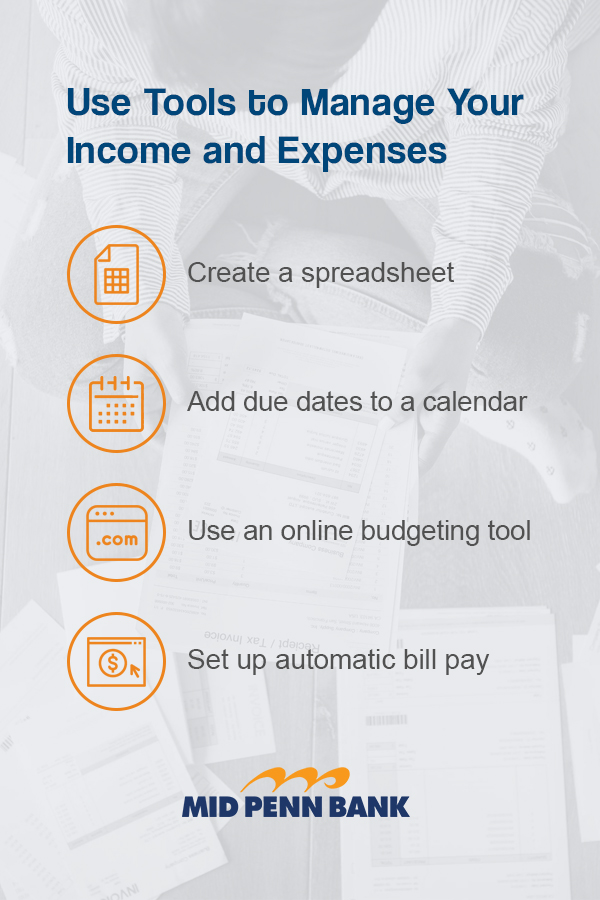

6. Use Tools to Manage Your Income and Expenses

You don’t have to try to keep track of your monthly earnings and expenses in your head, nor do you have to rely on pen and paper to record your bills and income. A variety of money management and budgeting tools are available to you, many of them for free. From creating a spreadsheet to setting up online bill pay, here are a few tools to use to help you manage your bills.

- Create a spreadsheet: You can use a spreadsheet to record your income, track expenses and record monthly payments and other costs. If you and your partner share expenses and income, you can use a shared spreadsheet so both of you can keep track of your bills.

- Add due dates to a calendar: If you sometimes forget to pay bills, an online calendar can help you keep track of due dates and send you a notification before each bill is due. You can program your bill due dates into the calendar as a recurring event, so a reminder about the due date pops up monthly.

- Use an online budgeting tool: Many apps and programs exist to help you keep track of your bills and other monthly expenses. It might take some trial and error before you find an app that works best for you. It can be worthwhile to try out a few and pick the one you find easiest to use, and that helps you take better control of your finances.

- Set up automatic bill pay: Online bill pay programs let you schedule recurring payments, meaning you don’t have to worry about missing a due date or paying late. You can also add payments manually if you want to make sure you have money in your bank account before a payment gets sent.

Tips to Help You Manage Your Bills

As you get in the habit of scheduling bill payments and get better at managing monthly expenses, the following tips will help you master your money and the bill-paying process.

1. Create a Physical Space for Managing Your Bills

Disorganization can get in the way of timely payments. If you often find yourself scrambling to find a bill or are unsure if something got paid, it can be helpful to carve out a physical space where you take care of all your bills. Even if you get e-bills, you might find it easier to have a physical, printed copy of each bill. Keep bills in the same spot, such as a filing cabinet or a basket on your desk.

Once a month, sit down and sort through the bills. Either pay them or mark them as paid if you use online bill pay and record the payment on your spreadsheet or budgeting app. Then, file the bills away so that you are ready for the next month.

2. Figure out How to Handle Irregular Expenses

Some expenses only come up once or twice a year or quarterly. Your auto insurance payment might be due every six months, or you might need to pay membership dues to an organization once a year. Irregular expenses have a way of surprising people.

A simple way to handle those non-monthly expenses is to figure out how much each one costs each month and treat them as monthly expenses. If your auto insurance is $60 every six months, plan to set aside $10 per month so you have the money to pay for it when the bill comes.

3. Use Cash When You Can

More and more people are using cards to pay for purchases. Between 2015 and 2016, the number of card payments increased by 7.4%. Using a card, whether it’s a debit or credit card, has its advantages. You don’t have to count out change, and the transaction is usually shorter.

But paying with cash reminds you that you’re paying for something with money, usually money you worked hard to earn. Paying with cash can make you think twice before buying something. To help yourself cut down on frivolous purchases or spending on non-necessities, you might find it useful to put yourself on a cash-only diet.

4. Talk to Your Partner about Financial Matters

If you’re married or share income and expenses with a partner, it’s essential that you both get on the same page when it comes to your bills and other financial concerns. You might find it helpful to assign one person the role of paying the bills, or you might divvy up your household bills and have each person take responsibility for a few. Keeping the lines of communication open about who’s paying what and when will help you both avoid missed payments and avoid duplicate payments.

Managing Your Monthly Expenses and Bills Helps Set You up for Financial Success

Managing your bills doesn’t only help you avoid the headache of missed payments and late fees. It can often be the first step on the path to financial success. When you know where your money is going and how it’s going to get there, you can start planning for the future and setting financial goals that look beyond bill payment, such as saving for a house or planning for retirement.

At Mid Penn Bank, we have been offering personalized service to our neighbors in Pennsylvania since 1868. Contact us to learn more about how we can help you build a foundation for your financial future.

View Our Personal Banking Options Open An Account Online Today

Share:

Disclosures

The material on this site was created for educational purposes. It is not intended to be and should not be treated as legal, tax, investment, accounting, or other professional advice.

Securities and Insurance Products:

NOT A DEPOSIT | NOT FDIC INSURED | NOT BANK GUARANTEED | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | MAY LOSE VALUE