How to Make Sure You Don’t Get Scammed at an ATM

Is your debit card safe? ATM scams are on the rise, according to data collected by the Fair Isaac Corporation (FICO). In 2016, the number of debit cards compromised at ATMs grew by 70%. That same year, the number of compromised card readers increased by 30%. Between 2016 and 2017, ATM fraud rose 10% and it was ranked as the third most pressing concern among financial institutions in 2017. ATM fraud and card theft cost financial institutions an average of $600 per card

FICO attributes the increase in ATMs scams to an increase in ATM scamming devices, such as skimmers. It’s easier than ever before for thieves to get their hands on such devices, and more and more people are doing just that.

The good news is it’s also relatively easy to protect yourself, your cards and your money. Here’s how not to fall victim to scams and theft at an ATM.

How Can You Recognize ATM Scams?

It’s important to know how to tell if an ATM has been tampered with. Knowing what to look for when you visit an ATM will help you avoid becoming a victim of a scam. Thieves use a variety of techniques to get your debit card number and PIN. Knowing how to spot the devices and tools a fraudster might use to get your debit card information is one way to protect yourself from theft. The next time you go to use an ATM, here’s what to keep an eye out for:

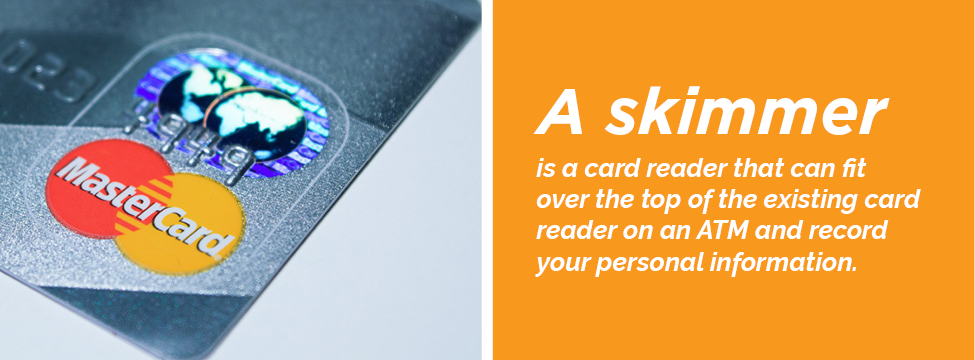

1. Card Reader Overlay

ATM thieves often use skimming devices to collect the information stored on ATM and debit cards, including card numbers and PINs. A card reader overlay is one of the most common examples of a skimming device. Card-reading skimmers are also pretty inexpensive, costing just a few hundred dollars on average. That makes them affordable for most thieves, especially if those criminals stand to gain thousands of dollars from stealing other people’s money.

A card reader overlay fits on top of the existing card reader on an ATM. When you swipe or insert your card into the machine, the skimmer reads and records the number. Usually, you can use the compromised ATM to get money or check your account balance without issue, so you might not even realize the skimmer is there if you’re not looking closely.

Although skimmers are often found in the ATMs themselves, some thieves are a bit more clever. They might install the skimmers on the device you need to swipe to get into an ATM vestibule after hours. Others use handheld skimmers to swipe people’s cards on the sly.

For example, a dishonest waiter or a thief posing as a waiter at a restaurant can take your debit card to pay for your meal. Instead of bringing the card back to the restaurant’s point of sale system right away, the thief can swipe it through the skimmer.

Once thieves have collected enough card numbers, they can produce fake debit cards featuring those numbers.

The next time you go to use an ATM, look closely at the card-reading slot. If you notice that anything looks strange, such as glue or tape near the card reader or a reader that seems loose, your best bet is not to use that particular machine. If possible, let an employee of the bank or store where the ATM is located know that you think something is up.

2. Hidden Cameras

You might be thinking, “a thief can use a skimmer to get my debit card information. But, he or she still won’t have access to my PIN!” Thieves often install a hidden camera on or near the ATM, along with the card reader overlay. The camera is usually pointed at the keypad and records your PIN as you type it in.

Hidden cameras are meant to be, well, hidden, so they can be tricky to spot. One thing to look for is a box that seems out of place. The box might be next to the ATM’s screen or to either side of the keypad. If you see a box, feel along its sides and corners, looking for a hole. Often, the hole will be pointed at the keypad, giving the camera tucked away inside a clear view of the keys.

3. Keypad Overlays

Hidden cameras aren’t the only method scammers use to record your PIN. Some also install a fake keypad, or a keypad overlay, on top of the real one. The additional keyboard can record your PIN as you put it in.

Often, you can tell that a keypad overlay is in place by feeling the keys on it. If the keys feel thicker than usual or spongy, your best bet is to stop using the ATM before entering in your entire PIN.

4. “Helpful” Thieves or Shoulder Surfing

Some thieves like to use a mix of modern and old-school techniques when stealing people’s ATM information. They might install a skimmer on the machine. But instead of using a camera or a fake keypad to record PINs, they will look over your shoulder as you type in your PIN.

In some cases, a thief might act like an innocent bystander, someone who’s just passing by and who noticed you were having trouble with the machine. It’s always a good idea to be wary of anyone you don’t know when you’re using an ATM, no matter where that ATM is located. If a stranger offers to help you with the machine, just say no thanks and leave. You can also report any suspicious behavior to the bank.

5. Card Trapping

Some thieves don’t want to go through the hassle of creating a new card from the stolen card number. Instead of installing a skimmer on an ATM, they might install a device that traps your card in the machine. You put your card into the slot and instead of processing your transaction, the machine seems to “eat” it, and you get an error message.

The thief may or may not also get your PIN by filming it with the hidden camera or through a false keypad on top of the real deal. Once you walk away from the machine, the thief will drop by and remove your card from the trapper.

6. Cash Trapping

Cash trapping is similar to card trapping. The big difference is the person using the device gets the cash you were trying to take out of the machine, rather than your card. You might get a message on the machine that the transaction didn’t go through, or you might just think the machine is broken since no cash comes out.

When you leave the area, the thief will come by to take the money out of the trap. Usually, cash trapping is less valuable to thieves than getting card numbers, but it also provides them with money immediately.

7. Shimmers

EMV chips make card reader skimmers pretty much worthless since the skimmers are designed to read the magnetic stripe on a card. To keep up with the changing times, some thieves have started to use “shimmers” at ATMs instead of card reader overlays. The shimmer captures the data on a chip-card, allowing a thief to produce a magnetic stripe card from it.

A shimmer slides into the ATM and is often not visible from the exterior, which can make spotting a compromised ATM tricky. Fortunately, a shimmer will only work if the EMV technology isn’t properly implemented in the ATM. Every time you use a debit card with an EMV chip, the card creates a new card verification value (dynamic CVV) for the transaction. Dynamic CVV is only good for a single transaction, meaning a counterfeit magnetic stripe card made with a dynamic CVV wouldn’t work.

8. Fake ATMs

Another way a thief can get access to card information is to install a “fake” ATM in a public place. Think about all the places where you might find an ATM, such as the corner of a gas station or a deli. Some ATMs are even located in restaurants or malls.

Although it takes considerably more effort to install a counterfeit ATM than to use a software program or skimmer, some thieves have done it. When you try to use your card at the machine, it gives you an error message and no cash after you’ve put in your PIN. Meanwhile, the thieves have been able to record your details.

9. ATM Deposit Scams

Here’s an old-fashioned way scammers can take advantage of you at an ATM. A thief will put an out-of-order sign on an ATM. Near the ATM, he or she will leave a box, instructing people who were going to deposit into the ATM to put their envelope in the box so a “teller” can collect the deposits and manually enter the transactions later.

The goal here is to steal any checks or cash people might be foolish enough to put into the box. If you are planning on depositing at an ATM and see an out-of-order sign, bring your cash or check into the bank or use your mobile app to make the deposit instead.

How Can You Protect Your Debit Card and Prevent ATM Fraud?

Although ATM scams and debit card theft are on the rise, the good news is you can be proactive about protecting yourself and your bank balance. Now that you know how to tell if an ATM has been tampered with, you are less likely to fall victim to ATM scams. The other good news is that the use of EMV-chip debit cards has seemed to slow down the rate of ATM fraud somewhat.

Until ATM fraud really is a thing of the past, though, there are several things you can do to prevent ATM scams:

- Choose your ATM with care. Some ATMs are better than others. It’s unlikely a thief will have installed a counterfeit ATM at your bank, and it’s unlikely that someone will have stuck a skimmer on an ATM inside your bank. Try to use the same ATM every time you need cash. That way, you know what it looks like and can quickly detect any changes.

- Inspect the ATM before using it. Whether you’re using a familiar ATM or not, give it a good inspection before you swipe or insert your card and before you put your PIN in. ATMs are pretty solid machines. If you notice the area where you put your card is loose or the keypad feels wobbly, don’t use the machine. If there are two machines next to each other, compare the two. If one looks considerably different from the other, that can be a sign one was tampered with. Also, look around and make sure the ATM has recognizable bank or card logos on it, such as the Visa or Mastercard logos.

- Be suspicious of out-of-order signs: Sometimes, if a thief has gone to the trouble of tampering with an ATM, they might put out-of-order signs on neighboring machines, to encourage people to use the tampered ones. If you see an out of order sign or any signs directing you to one machine over the others, your best bet is to find a different ATM.

- Keep an eye on your surroundings. Don’t go up to an ATM when someone else is hanging around it. Wait for the person to leave, keeping your distance. You can also come back later. Try to use an ATM that is in the middle of a busy area so someone can’t sneak up behind you.

- Cover your PIN. When you put your PIN in, cover the keypad with your free hand so a person can’t “shoulder surf” and memorize your number.

- Call your bank if you have any trouble at an ATM. If an ATM does eat your card or doesn’t give you the cash you withdrew, call your bank immediately. Don’t leave the ATM area while you call. You don’t want to give the thief a chance to swing by and take your card or cash.

- Pay attention to your bank balance. While keeping an eagle eye on your bank balance won’t keep someone from stealing your money, it will help you see right away when theft does occur. The sooner you report the theft to your bank, the better.

- Lower your daily withdrawal maximum. Most debit cards have a maximum daily withdrawal amount, meaning you can only take out a few hundred dollars per day. You might consider lowering that amount if you don’t regularly need to take out large amounts of cash. Doing so will limit the amount a scammer can swipe from your account during a day.

- Create a separate bank account for your debit card. Another way to protect your money from scammers is to create a dedicated checking account for cash and certain spending. Instead of putting all your money in the account, put only what you need for certain purchases in it. That way, you won’t lose all your money if your card is compromised. You’ll still have to wait for your bank to refund the money after the theft is reported, but the sting should be reduced somewhat.

Will EMV Cards Reduce the Risk for ATM Scams?

Cards that have the little chip in them, known as EMV cards, are meant to reduce the risk of fraud and theft. When you use a card that has a chip in it, it creates a one-time use code for the transaction, rather than using your card’s number.

In some ways, chip cards are safer than traditional magnetic stripe cards. But they aren’t a foolproof way to protect you from ATM scams.

For example, some thieves have tried using devices known as shimmers, which read the data on the card’s chip, making it possible for them to copy the card. If your card issuer reads the card verification value (CVV) when confirming the transaction, a shimmer won’t be able to steal the data on your chip. Not every issuer reads the CVV, which can put some card holders at risk.

If you’re concerned about shimmers, you can use the same techniques you would use to avoid skimmers and other scams. Cover the keypad while typing in the PIN, don’t use unfamiliar ATMs in out-of-the-way areas and pay close attention to your account balances.

What to Do If You’re a Victim of ATM Fraud

Sometimes, ATM fraud and theft happens despite your best efforts to prevent it. If you’ve been the victim of an ATM scam, you’re not necessarily out hundreds or thousands of dollars. The sooner you report the theft of a debit card, the less you’ll be on the hook for, per the Electronic Fund Transfer Act.

For example, if you report a debit card as lost or stolen before someone else uses it, you’ll be liable for $0. But if someone does use your card before you report it as stolen, you might be responsible for up to $50 worth of theft if you reported it within two days. If you wait longer than two days but report within 60 days, you can be responsible for up to $500.

If you don’t report your card lost or stolen within 60 days, then you are responsible for all the loss in your bank account, including any overdraft charges.

If you didn’t lose your card but you notice a transaction you didn’t make on your bank statement, you have up to 60 days to report the transactions to your bank. The sooner you report anything suspicious, the sooner your bank can cancel your debit card and keep the scammer from stealing anything else.

Bear in mind that your bank might have different rules than those outlined in the Electronic Fund Transfer Act. For example, your bank might provide zero liability protection, even if you don’t report your card lost or stolen right away. That can be especially helpful if you’re the victim of a skimming attack and don’t even realize your information’s been taken until a few days later.

Keep your bank’s contact information handy so you can easily get in touch to report any suspected fraud or theft. It’s also a good idea to have a phone number for your bank programmed into your phone so you can report any suspicious looking ATMs or any unusual ATM activity immediately.

Share:

Disclosures

The material on this site was created for educational purposes. It is not intended to be and should not be treated as legal, tax, investment, accounting, or other professional advice.

Securities and Insurance Products:

NOT A DEPOSIT | NOT FDIC INSURED | NOT BANK GUARANTEED | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | MAY LOSE VALUE