How to Protect Yourself From Identity Theft

When someone else uses your personal information without your permission, that constitutes identity theft. Identity theft can take multiple forms, from using someone’s credit card without their permission to opening credit cards or bank accounts in someone else’s name. Tax fraud and opening new mobile phone accounts are other examples of identity theft. In 2019, identity theft was the most commonly reported complaint to the Federal Trade Commission (FTC). The FTC received more than 650,000 complaints of identity theft in 2019, with credit card fraud being the most frequently reported type of identity theft. Reports of credit card fraud increased by 88% from 2018.

If you want to save yourself the stress and hassle of having someone else get their hands on your personal information, there are ways to protect your credit card information and personal details. Knowing how to keep your identity safe online is the first step toward preventing the misuse of your personal information.

How Can Your Personal Information Be Accessed by Others?

Part of learning how to keep credit card information safe is understanding how that information can fall into the wrong hands in the first place. A variety of techniques can be used to gain access to your private information. Some of the most commonly used tactics include:

- Sending phishing emails and phone calls: Your bank or credit card company will not send you an email requesting your personal information, such as your account number, PIN or password. They won’t call you requesting that information, either. But someone who wants to steal your information might try to call you or email you to get that information. Your best bet if you get a weird email or phone call from someone claiming to be from your credit card or bank is not to respond. If you want to verify the message, call the bank separately, using the number on your statements, not the number contained in the email or phone message.

- Digging through the trash: If you still receive paper statements or other documents with personal information on them, shred the paperwork or make sure you black out any private information on them before you toss them in the recycling bin or trash, to help keep your private information safe.

- Using malware and spyware: Software such as malware or spyware can give unauthorized individuals or organizations access to your information. The software can track your keystrokes and record your personal information. Malware can get on your computer, tablet or smartphone in a few ways. If a website isn’t properly protected, someone can adjust its code so that the malware gets downloaded when people visit the site. Malware can also hide in downloads that seem legitimate. If you’re not sure of the source of a file, it’s a good idea not to download it.

- Accessing companies’ data: Data breaches reveal confidential information to individuals who can use it for nefarious purposes. A data breach occurs when someone discovers vulnerabilities in a company’s security and attacks those vulnerabilities and gains access to information that should be secure.

- Installing card skimmers: A skimming device, installed at the point of sale, collects information from credit or debit cards. A skimmer sits on top of the card reader on a credit card machine or ATM. When you insert your card into the machine, the skimmer reads it and sends the information to the individual or group that is committing identity theft. In some cases, it can be very easy to see that a skimmer has been installed on a machine, as the devices can be clunky or look out of place.

- Intercepting public WiFi: Free public WiFi can help you avoid using up your phone’s data, but can also put your personal information at risk, as the information sent over the network can be intercepted. Your best bet is not to enter any personal information or credit card info when using a public, non-password-protected WiFi network. Wait until you’re on a secure network or using your phone’s data to make purchases or look up your bank information.

Credit Card Safety Features

The good news is that credit cards have built-in security features that are designed to limit the risk of fraud. The features range from liability protection and transaction monitoring to encrypting information, so a third party can’t access it. Some of the most common security features of credit and debit cards include:

- Signature panel: The back of every credit and debit card has a signature panel, which needs to be signed by the owner of the card. A credit or debit card technically isn’t valid without a signature. The system isn’t perfect though, as many merchants will accept a card that isn’t signed or won’t even check to see that the back of the card is signed before completing the purchase.

- Card Verification Value (CVV): Along with the 16-digit account number and expiration date, most credit and debit cards also have a three or four-digit CVV printed on the back. The CVV is meant to provide an extra layer of security, particularly when you use the card for online or over-the-phone purchases.

- Single-use numbers: Many credit card issuers will provide single-use card numbers for people to use when shopping online. A single-use card number is only good for one transaction, so even if a third party manages to intercept the number through malware or a data breach, it wouldn’t be of much use to them.

- EMV chips: Today, nearly all credit and debit cards feature a small computer chip built-in, known as an EMV chip. The chip creates a single-use code every time you use the card. Compared to magnetic stripes, they are much more secure, as someone who intercepts a transaction only gets access to the one-time-use code and not the credit card number itself. EMV chips can help to prevent identity theft and fraud when you use a card at a store, but don’t offer extra online credit card payment security.

- Monitoring: Although not a feature built into the card itself, most banks that issue credit cards monitor transaction activity and will contact you when they notice any unusual activity. In some cases, the activity might just be you making multiple purchases all at once, or when you use the card when traveling. In other cases, the activity might be because someone has gotten access to your card number.

- Virtual card numbers: A virtual card number is separate from the number printed on your physical card and is usually stored in an online wallet. Although the number is connected to your card, it’s easy to delete it if there’s a data breach or if you lose your smartphone or another mobile device.

- Fraud protection: If someone does get access to your credit card, the maximum amount you’re liable for legally is $50. Many credit card companies offer $0 fraud liability protection, meaning you don’t have to pay for any unauthorized use of your cards.

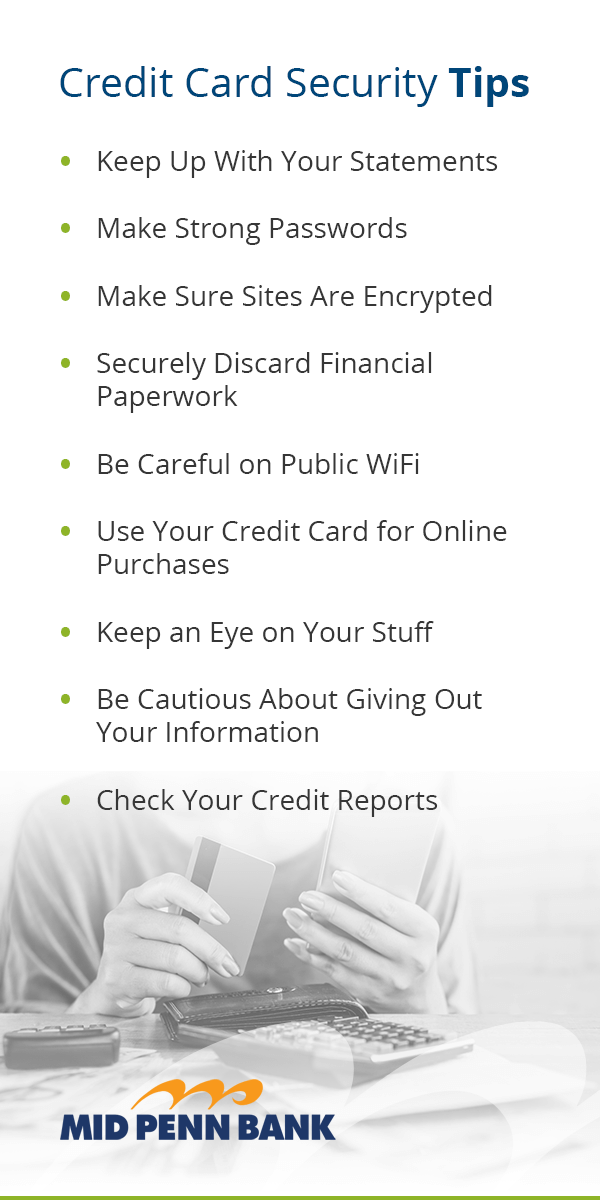

Credit Card Security Tips

Identity theft can happen, but it’s not inevitable. Here’s what you can do to keep your credit card information safe online and to protect your personal information.

1. Keep Up With Your Statements

Your credit card and bank send you statements at the end of each month, listing all of your transactions and any amounts you owe. It’s a best practice to review your statements carefully, keeping an eye out for any purchases or withdrawals you don’t recognize.

You can also check on your accounts throughout the month by utilizing credit card mobile apps, or logging into online or mobile banking. This can help catch unauthorized transactions as they happen. The sooner you find and report any unauthorized purchases, the sooner you’ll get your money back or the fraudulent purchase reversed.

2. Make Strong Passwords

Strong passwords are harder to guess or crack than simple passwords. When making a password to use for your bank account, credit card account or other financial accounts, get creative. Use a mix of letters, numbers and special characters. The longer the password, the better. You might want to think of a phrase to use as your password rather than a single word followed by a string of numbers. You can replace some letters with numbers to make it harder to crack.

Along with making your passwords strong, be cautious about where you store them. Many web browsers will offer to save your passwords for you, so it’s easier to log in the next time you need to access your account. But if you save passwords on the browser, anyone can get into your accounts when they use your computer.

It’s also a smart idea to change up your passwords regularly. Some websites will automatically prompt you to do so every few months. If they don’t, it can be worthwhile to get in the habit of changing your passwords at the beginning of each season, such as on the first day of spring, summer, fall and winter.

3. Make Sure Sites Are Encrypted

Many shopping and financial websites are encrypted, meaning the data that gets sent is masked so that it is difficult for anyone who intercepts it to figure out what it means. There are two ways to tell if a website is secure and encrypted. One way is to look for the “s” at the end of “http” at the start of the site’s URL. You can also look for the padlock icon in the URL bar.

If a website doesn’t use https and doesn’t have the padlock, your best bet is to avoid providing any personal information while using it.

4. Securely Discard Financial Paperwork

A third party can sometimes get all the information they need from bank and credit card statements you’ve thrown out or from other financial documents. If you still get paper statements, bills and other documents mailed to you, be sure to either shred the paperwork before you recycle or discard it or use a marker to black out all personal information.

5. Be Careful on Public WiFi

Be extra cautious when using any public WiFi networks. If you send any information through a site that’s not encrypted on a non-password-protected network, someone else can intercept your details. It’s safest to avoid any transactions that would require you to reveal personal information when using an unprotected, public network.

If you need to be on a public network, you might want to install a virtual private network (VPN) on your device first. A VPN will create an encrypted connection and will mask your IP address, so it’s nearly impossible for others to spy on what you’re doing.

7. Keep an Eye on Your Stuff

Another way to protect your personal information is to keep a close eye on your belongings. When you’re out and about, keep your wallet and smartphone close to your body at all times, so that they are harder to steal. If you use a laptop in public, make sure it stays by your side. It’s also a good idea to password-protect your devices, so the information you store on them cannot be accessed.

8. Be Cautious About Giving Out Your Information

The odds of your bank or credit card company calling you to ask for your account number or other personal information are slim to none. They also won’t email you to ask for those details. If you get an unusual call or email, your best bet is to ignore it. It’s also a good idea not to click on any links in emails that seem to be from a financial institution.

9. Monitor Your Credit Reports

Identity theft can occur when someone takes your personal information and uses it to open new accounts, such as a new credit card or personal loan. Checking your credit report throughout the year can help you detect any suspicious or unauthorized new accounts and enables you to take action quickly. The three credit bureaus, Equifax, Experian and TransUnion, will each allow you to check your credit for free, once a year.

What to Do If You Become a Victim of Identity Theft

If someone does steal your credit or debit card number or otherwise gets access to your personal information, it pays to act quickly to keep your credit safe. The first thing to do is close any affected accounts. Your credit card issuer will cancel your current card number and give you a new one. Your bank will create a new checking or savings account for you. Once you’ve closed the affected account, be sure to update any direct deposits or auto-payments.

Next, get in touch with one of the three credit bureaus — Equifax, Experian or TransUnion — and ask them to put a fraud alert on your file. You only need to reach out to one bureau to have the alert put on each of your three files. With a fraud alert in place, a creditor needs to take extra steps to verify your identity before it can issue you a new loan account. It’s also a good idea to let the IRS know about any fraud, so it can keep an eye on your account for anything suspicious, such as a fraudulent tax return.

Review your credit reports, looking for any accounts you didn’t open or other suspicious activity. You can also sign up for credit monitoring, so you get notified if anyone tries to open a new account in your name.

Finally, it’s a good idea to let the police know what’s happened, and to report your issue to the FTC. Filing a police report creates a paper trail that can help you down the line. It also helps the authorities notice crime patterns and can help them find the person responsible. Although the FTC won’t directly intervene on your behalf, it does provide the information it gathers to law enforcement, such as the Pennsylvania Office of Attorney General. Law enforcement can then use the information gathered to identify trends and more effectively do its job.

Mid Penn Bank Can Help Keep Your Identity Safe

Mid Penn Bank has been serving residents of central Pennsylvania since 1868. We offer checking accounts, savings accounts, credit cards and a variety of consumer and commercial loan products. As a member of the local community, we are committed to keeping your personal information safe.

Our debit cards employ technology to help prevent fraud. As a Mid Penn Bank account holder, you also have access to Card Controls. Card Controls is a mobile app available for both Apple and Android devices that allows you to control the use of your debit card, increasing security measures and further preventing fraud. From the app, you can easily and quickly turn your debit card on and off, set spending limits, control the geographic areas your card can be used in, and even set spending limits by retailer categories!

CardValet has even more options available to help you ensure your debit card and corresponding account are protected from identity theft and fraud. Mid Penn Bank Visa and American Express credit cards also contain numerous built-in safety features to help your identity and your credit to be as protected as possible.

To learn more, contact us today using our secure online form.

Share:

Disclosures

The material on this site was created for educational purposes. It is not intended to be and should not be treated as legal, tax, investment, accounting, or other professional advice.

Securities and Insurance Products:

NOT A DEPOSIT | NOT FDIC INSURED | NOT BANK GUARANTEED | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | MAY LOSE VALUE