Yes, Everyone Can Save Money: 5 Ways to Build Your Savings

Across the U.S., people are getting better at saving their money. In 2018, 61% of adults said they could cover a $400 emergency using cash or the equivalent. This number was up from 50% in 2013. In July 2020, the personal savings rate — the amount of disposable income people save, rather than spend — was 17.7%. This number rose from 7.2% in December 2019.

If you are not currently saving money or would like to increase the amount you set aside for a rainy day, you can —even without getting a raise. Consider your goals and evaluate how you spend money to find where you can make changes to get your savings on track. Ask yourself what steps you’re willing to take to increase your savings account.

Continue reading to learn how to set aside money for savings.

Choose the Right Tools for Your Savings

Before you start thinking about ways to build your savings, it’s worthwhile to brush up on the options available to you. You can deposit your cash in several types of accounts, each with unique benefits and potential drawbacks. Some types are more secure than others, as they are protected by the Federal Deposit Insurance Corporation (FDIC). FDIC-protected accounts will not lose value, even if the bank that holds them fails. Your reasons for saving money can also influence where you put your money.

The following are some options to consider:

1. Personal Savings Account

Money in a personal savings account earns interest. This means your account’s value grows over time as long as you leave the money in it. Personal savings accounts are FDIC-insured for up to $250,000 per account. Money kept in a savings account is also relatively liquid. You can withdraw it when you need to, without having to pay a penalty. Although some accounts do charge a monthly fee, free savings accounts are available.

2. Certificate of Deposit

A certificate of deposit (CD) is similar to a personal savings account in some ways. The money in a CD is FDIC-insured and earns interest. Often, the interest rate on a CD is higher than the rate offered on a personal savings account. This is because you need to leave the money in the CD for a set amount of time, such as six months or 12 months. CDs often charge an interest penalty, such as three months of interest, if you need to close the account early. If you don’t expect you will need easy access to your cash for several months or a year, a CD can be a good savings option.

3. IRA Savings Account

An individual retirement account (IRA) helps you set aside money for retirement in addition to a 401(k) or similar plan you may have from your employer. One way to save with an IRA is by putting money into a savings account. Like a personal savings account, an IRA savings account earns interest. Money in an IRA savings account is FDIC-insured. A notable difference is when you can access the money in an IRA account and its tax treatment.

If you open a traditional IRA account, you don’t pay income tax on the annual contributions you make to it. Tax is deferred until you withdraw from the account during retirement after age 59 1/2. If you open a Roth IRA, you pay tax on the amount you contribute to the account. You won’t pay tax on the original amount or any earnings when you withdraw it at retirement.

4. Stocks or Mutual Funds

Stocks and mutual funds don’t earn interest. Instead, they can increase in value as the value of their shares increases. Some types of stocks or mutual funds also pay dividends to their investors. While stocks and mutual funds have the chance of earning a higher return on investment compared to savings accounts, they do not have FDIC protection.

The value of your saved money could drop if the value of your investment stocks drops. Usually, stocks and mutual funds are ideal for long-term retirement savings rather than emergency fund savings or other short-term financial goals.

Do You Need a Savings Account?

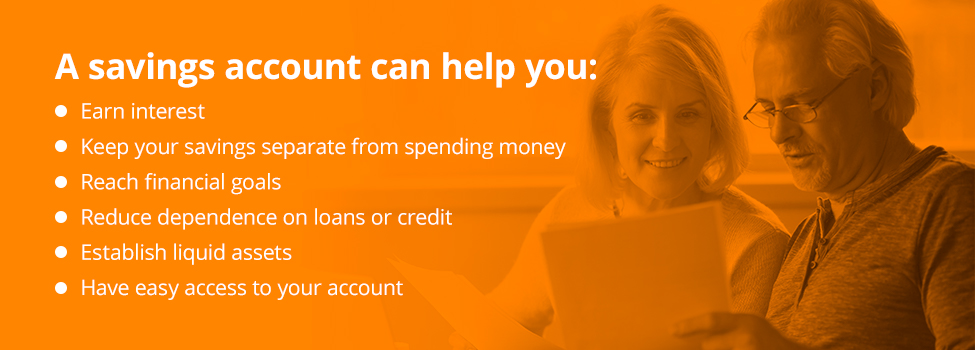

Savings accounts offer multiple benefits to people who are working toward financial goals. These goals may include saving for an emergency, building a down payment for a house, saving for retirement or saving for a child’s future education. A savings account can help you:

- Earn interest: Most savings accounts pay some amount of interest, and that interest usually compounds. The interest you earn ends up earning interest, helping to increase the value of the account.

- Keep your savings separate from spending money: When you open an account specifically for saving, you give your money a purpose. Putting the money you want to save in its own account can make you more likely to keep that money and reduce the chance that you’ll spend it.

- Reach financial goals: Opening a savings account that pays interest can help you reach specific financial goals, such as saving three months’ worth of expenses as an emergency fund or saving for a home down payment. You might find that opening separate accounts for each goal helps keep you on track.

- Reduce dependence on loans or credit: With money in savings, you may be less likely to rely on credit or personal loans when you have an unexpected expense. Instead of charging a car repair or medical bill to your credit card, you can use the money you have in savings to pay for the expense. Paying in cash or with money reserved in savings is often more affordable than charging purchases, as you won’t have to pay interest on the amount.

- Establish liquid assets: Though savings accounts have withdrawal limits and may restrict the number of times you can withdraw money from the account each month, they are more liquid than options like owning stocks or investing in real estate. You can access your money when you need to and don’t have to wait for a sale to go through. Savings accounts are FDIC-insured, which means they will only increase in value. You won’t have to worry about your account during a market slowdown or slump.

- Have easy access to your account: Online savings accounts make it easy for you to keep track of your money and monitor your account at any time and from anywhere you have an internet connection.

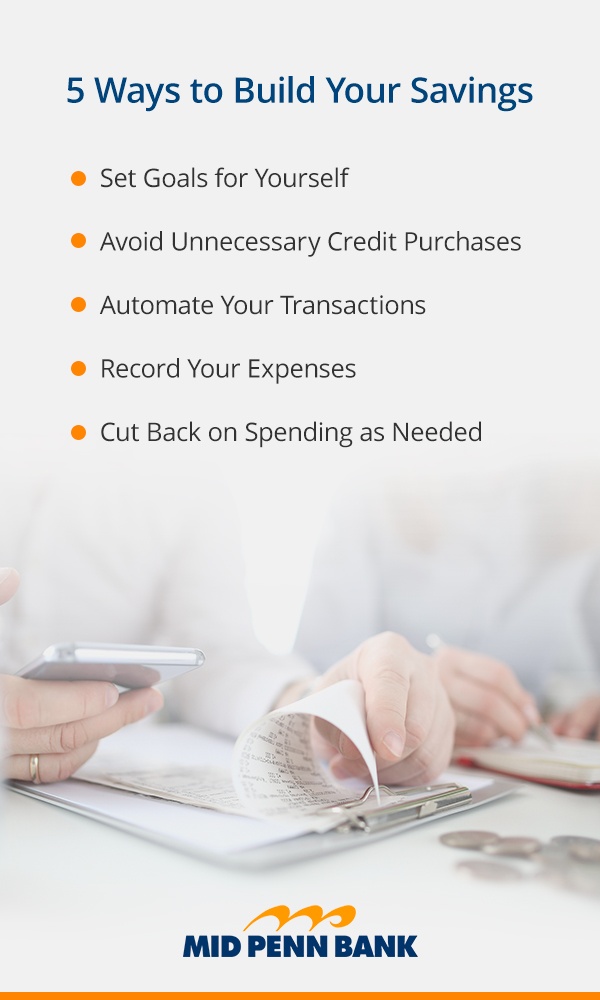

5 Ways to Build Your Savings

Opening an account is just the first step when considering ways to build savings. The next step is to put money into the account. You can make deposits into your savings accounts regularly, allowing them to build up over time. If you are having difficulty getting started, a few tweaks to your habits and mindset may help increase your savings rate:

1. Set Goals for Yourself

Establishing your motivation for saving money can help you remain committed to the practice. A clear “why” can help you understand the importance of saving while giving you something toward which to work. When you set financial goals, some things to consider include:

- The length of the goal: Financial goals can be long or short term. A short-term goal might be to save $1,000 in an emergency fund over the next 12 months. A long-term goal might be to save enough to retire comfortably at age 68.

- The target amount: How much do you hope to save? You might need to calculate some values to see how much money you’ll need. If you hope to save up six months’ worth of expenses as an emergency fund, how much do your expenses cost over six months? How much would you need to retire at your target age, based on your current income and spending habits?

- Where you’ll save: Consider where you’ll put the money you’re saving. A savings account is ideal for the money you need to access quickly. You might consider investing in stocks or mutual funds for longer-term goals, depending on your age and when you’ll need the money. The stock market is riskier than a savings account, but it also has the potential to earn a higher return.

- How much you’ll save each month: Figure out how much you’ll need to save monthly or on the schedule that works for you. To build up a $1,000 emergency fund over 12 months, you’d need to save around $84 per month.

2. Avoid Unnecessary Credit Purchases

A credit card can be more of a budgeting tool than you might think. When you use your credit card to pay for regular expenses, it may become easier to keep track of those expenses. Credit cards also offer protection again fraud and theft. If you have a rewards card, you can earn cash back on your regular purchases.

The goal is to avoid using your card to buy things you don’t need or didn’t plan on purchasing. Going over your budget or otherwise charging too much to your card makes it easy to go into debt. Try to charge only what you know you can afford to pay back before the due date. You can avoid interest and an increasing credit card balance this way.

The better you are with your credit use, the higher your credit score may be. With a high credit score, you can get better interest rates on loans and are more likely to be approved for a mortgage or other types of loans.

3. Automate Your Transactions

Once you’ve determined how much you want to save and where you’ll save it, automating the process as much as possible can help you stay on track. You can automate transactions in a few ways. If you have a 401(k) or another retirement plan through your employer, you can have your retirement contributions automatically deducted from your paycheck each pay period.

You can also set up your savings accounts to automatically transfer your target savings amount on the schedule that works for you. If you’re going to save $100 each month for your emergency fund, schedule a recurring transfer so the money moves from your checking to savings on the same day each month. You might set up the transfer so it takes place bi-monthly or occurs on the first or last day of the month.

When you automate your savings, you won’t forget to save during the month. You may also be more likely to reach your goals sooner when the process happens for you.

4. Record Your Expenses

Saving money becomes easier when you know how much you spend each month and how your spending compares to the amount you earn. Track your expenses for several months. You can keep track by recording your spending in a notebook, using budgeting software or creating a spreadsheet. Note everything you spend money on, even small purchases like a donut or coffee.

After tracking expenses for a few months, see how they compare to your income. If you spend more than you earn, it can be difficult to come up with the money to save. If you have disposable income left over each month, determine how you’ll allocate it to savings. It might help to focus on the most pressing issues first in your saving. Once your short-term savings is established, you can focus on longer-term savings.

5. Cut Back on Spending as Needed

A favorable scenario to find yourself in is having fewer expenses than income each month. For many people, the opposite is true. Their expenses are often greater than their income. In this situation, you may want to find ways to cut back. Ask yourself what you can eliminate from your spending every month. Instead of dining out, you might eat more meals at home. You might switch to a lower-cost internet service plan or start shopping at a budget-friendly grocery store.

Make enough lifestyle and spending adjustments to allow yourself the money you need to reach your spending goals. But try not to go too far overboard with your restrictions. If you cut out too many things, you might start to feel deprived. Feelings of deprivation can make it challenging to stay on track. Allow yourself some fun money each month, even if it’s only enough to cover the cost of a single streaming subscription, a weekly fancy coffee or a bi-monthly night out with friends.

Open a Savings Account at Mid Penn Bank Today

The first thing to do if you’re ready to start saving is to open an account. Once you open an account, you can begin to determine how to save money in your savings account. Mid Penn Bank offers personal savings accounts with no monthly fees and free online banking. Contact us today to learn more and to open your free savings account.

Share:

Disclosures

The material on this site was created for educational purposes. It is not intended to be and should not be treated as legal, tax, investment, accounting, or other professional advice.

Securities and Insurance Products:

NOT A DEPOSIT | NOT FDIC INSURED | NOT BANK GUARANTEED | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | MAY LOSE VALUE